Software innovation is usually seen as a improvement on existing processes. However, the critical software innovation is not incremental, it’s built like a ladder. Google is famous as an organization for shooting for the moon, and not investing resources on a project if it won’t deliver at least one order of magnitude improvements. These type of changes do not result in changes to existing processes, but rather the creation of new processes that altogether replace less efficient ones, disrupting the space of the incumbents.

We have an opportunity not only to improve existing processes and products, but to completely turn the existing market upside down — the ADAS, fleet risk management and insurance markets as a whole.

When Google started, the web was structured into large directories of pages, across Yahoo and AOL, curated by teams of expert editors. Web search was not deemed useful, as there was too much “stuff” in there, and the gems were hidden and hard to find. The industry believed that expert human editors were required to meticulously surf the web (“surfer dudes”) and find those gems. Audience came in to browse the directory and discover new content. Display advertising was born and became an extremely lucrative business of these publishers like AOL and Yahoo. Display advertising contracts guaranteed a premium audience and impressions to those advertisers, something that before had been confined to radio, TV and print media. And then Google appeared. Google realized it could not compete in web search with humans. The editor-curated directory was too good, and web search “head” queries were almost non existent. But the velocity at which the hidden gems were appearing on the directory was too slow. Google started to apply information retrieval techniques at very large scale to build a search index for the tail, using a crowd-sourced reputation model (aka PageRank) rather than head editors. The objective was (and is) to go as down the tail as far as possible. The better you could answer rare and complex queries, the better the user value of Google was. Because of this ability to continuously go down the tail, Google started to become the main way for users to find information. To the point that even head queries were now being resolved through search. By enabling more and more tail search queries, Google opened a new advertising marketplace: direct response. Whereas display advertising in the publisher directories was mainly about awareness and engagement driven by a short list of top 1000 advertisers, with billions of dollars each in marketing budgets, there were also millions of small and medium underserved businesses willing to spend a few hundred or thousands of dollars. They were no good customers for Yahoo or AOL: Yahoo would never spend the sales resources to target them, and small businesses would not consider Yahoo anyway since it did not provide the desired call to action and effectively CPAs. So by being able to finely target tail queries, Google found the way to open the market of direct response in sponsored search (in all fairness, it was Overture who invented sponsored search, but Overture did not have just deep index, which to Yahoo acquiring both Inktomi and Overture - just all a bit too late though).

The market dynamics are the same Google faced back in 2000. Similar dynamics, similar tactics to win.

In today’s world, automotive safety and risk management applications (ADAS, telematics, etc.) are developed very slowly, hand crafted to specific use cases, one by one. In the case of ADAS, a Forward Vehicle Collision Warning is different than a Forward Bicycle Collision Warning. Developing each of them requires craftsmanship, gathering data, labeling data, doing feature engineering and finally deploying into the field. The development process is high-touch, and extremely intense as an R&D portion of the P&L. But most importantly, it’s slow. Because of the need to justify higher revenue numbers, and because of the integration-drive nature of the incumbent automobile original equipment manufacturers –here Tesla being the exception–, automotive safety applications are packaged with hardware solutions. Hardware solutions take years to get into the vehicle and put up for sale. Altogether, the industry remains designed to be slow and expensive. Which leads us to size. With Intel acquisition of MobilEye in early 2017, we saw the leader of this (inefficient) market command 15 billion USD. This is the same situation Yahoo was in, by only targeting large advertisers, it missed the millions of small and medium businesses that also wanted to market their products. With MobilEye, and other ADAS players, targeting a thin segment of the top 3-5% of the automotive sales they have confined themselves into the head of the market, leaving the tail out for us to take on.

And like in search, solving for the tail of automated driving systems requires software innovation that will dramatically change the processes that build up this industry.

The game is to increase the velocity at which we solve tail use cases. How long will it take for an incumbent ADAS solution provider to design, build, test, and rollout an algorithm for detection of broken tire debris on the road and the consequent warning system for it, i.e. is it big enough for me to brake, or small enough that I can safely go over it? Or to warn about a police car on the shoulder? The tail of driving is long, much longer than search (the information gain in driving could in fact be considered to be infinite). Only if we build up the necessary velocity to solve this systematically we will win. The faster we go down the tail, the harder it will be for others to catch up. This ability to continuously learn at high velocity and improve our systems for the tail as our users drive more and more is in fact our core technological strategic tenet.

And it is exactly why by solving for the tail we will win our business. When individual commercial drivers, fleet owners, or even consumers, look at safety, they all have tail use cases in mind. These are all the small and medium businesses that were underserved by display advertising and the directory of pages. Will it an ADAS solution work with my Toyota Corolla 1999? Well, no, not really, as to make it work, there would need to be a customization project in regards to camera location, height of vehicle, braking horse power, etc. Could I get traffic light state detection? Again, no, not in the next 5 years … We know from the huge number of telematics solution providers out there that (1) there is a long tail of use cases that fleet owners need solving, and (2) the barrier of entry to solving each of them independently is low, but as a whole is impossible (as hence there is no market leader). By going after the tail, we open new markets and we move from a world of costly physical sales to online sales. Nexar’s automotive safety and risk management applications, build continuously for the tail, can uncap an enormous market across telematics, automated driving systems, and insurance underwriting worth well over a trillion dollars.

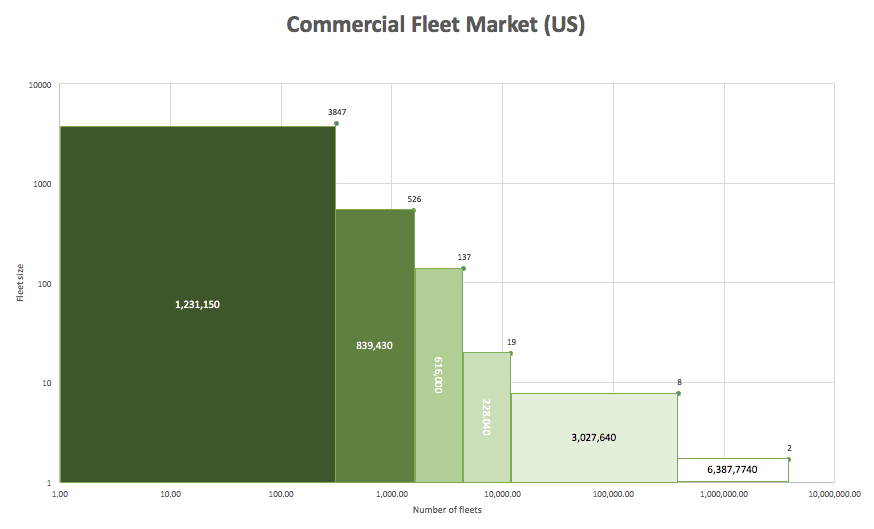

When we look at commercial fleets only (not personal vehicles / consumers), we see just this, a nice and long fat tail.

The market leaders in the vision safety apps space (ADAS, connected camera) control large fleets (500+). But when we expand to all commercial fleet and non-fleet sizes, from 1-499, we have a market, which none of these players address. The opportunity is huge, and this does not even take into account the remaining 250 million personal vehicles out there in the US.

Which is why, at Nexar, we work on the tail (product) for the tails (customers).